Competitive Strategies in Beverage Alcohol - November 2022

Latest report on competitive market strategies for the alcoholic sector published this morning! Some exciting things you need to know, including a great macro picture recap for various sectors.

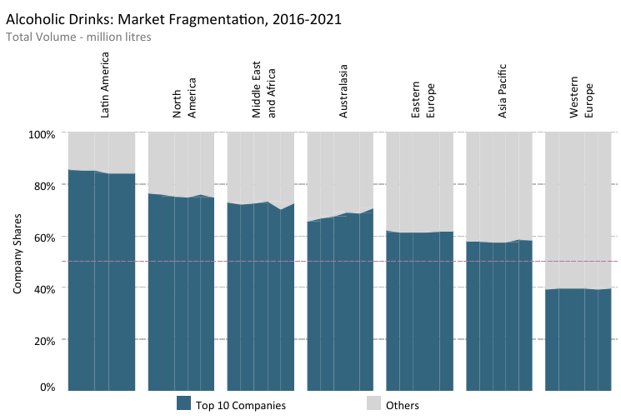

In general, an enthusiastic return to the on-trade supported recovery for alcoholic drinks players following the decimation caused by pandemic restrictions. However, the industry is now facing a host of challenges - macroeconomic and geopolitical upheaval, supply chain disruption, and ingredient and material shortages. The no/low alcohol sector, RTDs and the digital space remain dynamic. Few key data points to consider:

· Flexibility is more important than ever

o Companies are branching out beyond their traditional core focus areas in terms of products, alcohol content, price points and distribution and marketing channels as they seek to engage with new consumers across a wider range of occasions. Expansive portfolios covering economy to premium and above brands boost leading producers’ capacity to adapt, an important advantage in the current unsettled environment.

· Category lines continue to blur

o The boundary between alcoholic and soft drinks is becoming increasing less distinct - for both consumers and producers. Alcoholic drinks players’ growing involvement with the no/low alcohol sector is seeing them cross into soft drinks territory, while in the other direction, leading brand owners such as Coca-Cola and PepsiCo are launching alcoholic offers. Partnerships, joint ventures and acquisitions offer opportunities as diversification gains ever-greater strategic importance.

· Recovery faces significant setbacks

o Most international players saw volumes rebound in 2021 as the on-trade re-opened in the second half of the year in much of the world. Top players that are more reliant on one or two key markets in Asia Pacific were exposed to extended restrictions and case rate increases, negatively affecting growth. Although industry resilience remains evident, severe macroeconomic pressures could impede short- to mid-term performance.

· Digital developments accelerate

o The industry is embracing digital advances. Companies are exploring the range of possibilities in this space now that online channels have cemented their importance to sales and communication. Digital native brands are a growing focus for acquisitions and product launches, and engagement approaches are moving into the metaverse. Consistency and quality of experience will be key to successfully integrating the physical and digital worlds.